Drozd: Tweezer bottom signaled reversal in Nov. canola

By David Drozd

| 3 min read

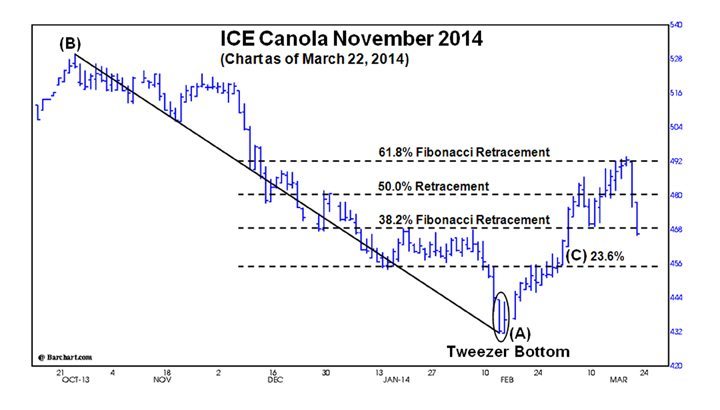

ICE canola, November 2014, as of March 22. (Barchart.com)

Canola prices on the November 2014 futures contract lost nearly $100 per tonne before retracing a percentage of those losses.

Four months after turning down from a high of $530 per tonne on Oct. 24, 2013, a tweezer bottom alerted savvy traders and farmers alike that the market was about to turn up.

A tweezer bottom materializes when the same low occurs for two consecutive days. In this case, the November futures posted a new contract low of $431.50 on Feb. 13 and 14, 2014. A tweezer bottom is a reversal pattern seen at market lows and it is especially reliable when it develops at the bottom of a major decline.

When the tweezer bottom occurred, farmers were calling us and asking, “How high?” To answer that question, I turned their attention to the charts to indicate the fibonacci retracement levels.

Fibonacci retracement

This is a popular tool used in technical analysis based on key numbers identified by mathematician Leonardo Fibonacci in the 13th century. A fibonacci retracement is the potential correction of a market’s original move in price. In a downtrending market, this refers to areas of resistance where prices have the potential of rallying to before they resume their downward progression. This is advantageous for canola growers to know, so they can determine targets for making a sale.

As illustrated in the accompanying chart, the 61.8 per cent fibonacci retracement level was $492.40, 50 per cent was $480.80 and 38.2 per cent came in at $469.20. A market typically has a 38.2 to 61.8 per cent retracement. It is important to note that downtrending markets such as canola rarely have more than a 61.8 per cent retracement.

Fibonacci retracements use horizontal lines to indicate areas of resistance at key fibonacci ratios before a market continues in the original direction. These levels are created by drawing a trendline between two extreme points, identified as (A) 0.00 per cent, the start of the retracement, and (B) a 100 per cent retracement of the original move, and then dividing the vertical distance by the key fibonacci ratios of 23.6, 38.2, 50 and 61.8 per cent. The two extreme points were (A) $431.50 on Feb. 14, 2014 and (B) $530 on Oct. 24, 2013.

While minor 23.6 per cent retracements do occur, the most common fibonacci retracements are 38.2 and 61.8 per cent, with 50 per cent being in the middle. The 50 per cent retracement level is not really a fibonacci ratio, but it is used because of the tendency for a market to continue to the 61.8 per cent retracement level, once it completes a 50 per cent retracement.

Market psychology: A tweezer bottom signals an abrupt change in trend. Traders who were short the market quickly questioned the market’s strength, as prices challenged the first area of resistance at $454.80. After all, nothing had changed fundamentally, with Canadian ending stocks of canola expected to be record high in 2013-14.

However, markets have short covering rallies to alleviate the oversold conditions. Once prices exceeded $454.80, which was the 23.6 per cent fibonacci retracement level, the market ran into buy stops a few dollars above that point of resistance (C).

Buy stops are placed above the market, typically just above a key point of resistance to protect the profit of those who shorted the market at higher levels. Once triggered, they become orders to buy at the market, driving prices up until willing sellers are uncovered.

This buying quickly triggered additional buy stop orders when the market soared above the 38.2 per cent fibonacci retracement level. With the amount of buying overwhelming the available supply of contracts for sale, prices rallied to the 50 per cent retracement level. This now provided optimism that prices could rally to the 61.8 per cent retracement level.

Farmers who were interested in making an additional sale and targeted the 61.8 per cent retracement level were rewarded for their patience when prices achieved $492.40 on March 18, 2014.

Send your questions or comments about this article and chart to [email protected].

— David Drozd is president and senior market analyst for Winnipeg-based Ag-Chieve Corp. The opinions expressed are those of the writer and are solely intended to assist readers with a better understanding of technical analysis. Visit Ag-Chieve online for information about our grain marketing advisory service and to see our latest grain market analysis. You can call us toll-free at 1-888-274-3138 for a free consultation.